19 May Humans cause severe weather? Surprise!

It seems that we’re seeing or experiencing more frequent and severe weather events; and fingers are being pointed toward human activities (anthropogenic warming) as a contributing factor. Because of the human and economic devastation caused by severe weather, it is our nature to want to control these events if humans are considered a cause.

From an insurance perspective, we share the same desire whether it is controlling the causes or preventing damage. After all, insurance companies pay the bills and have the most money to lose when storms occur.

Our interest in the weather is a desire to minimize our customers’ losses when wind, lightning and water conspire to destroy property or threaten lives. So, are people causing problems or is something else going on?

A recent article in Carrier Management magazine discussed the data used by the Intergovernmental Panel on Climate Change (IPCC). This group is described as “the scientific body under the auspices of the United Nations that reviews and assesses the scientific, technical and socio-economic information produced by scientists around the world.”

Looking at data dating back to 1851, Karen Clark of Karen Clark & Co. (no relation), concluded that the frequency of tropical cyclones has not so much increased as has the ability to detect storms. She notes that until aircraft and spacecraft began spotting and tracking storms, most data was gathered by mariners which limited the number of their observations.

Her other conclusion was that loss of life and property has certainly increased over time but mostly as a result of more people and property being close to where storms make landfall. Also, the value of those properties has increased tremendously. Little coastal communities that once featured seasonal summer cottages now sport multi-million dollar “McMansions” with docks, outbuildings and other expensive improvements.

The article concludes that frequency of weather events and human activity have no meaningful correlation. However, the statistical modeling suggests that toward the end of this century, the severity of storms may, indeed, be influenced by warming of the oceans caused in part by humans. A storm’s intensity is a function of air and water temperatures. The article states, “According to the climate models, hurricanes could be more intense by the end of the 21st century, with maximum wind speeds 2-11 percent higher than the current reference period.”

Is that increase a big deal? Actually, it is.

The article goes on to state that “losses increase exponentially with wind speeds” so, a two percent increase in wind speed can produce a 10 percent increase is damage. If the wind speed increases by 11 percent, resulting damage may increase by 50 percent!

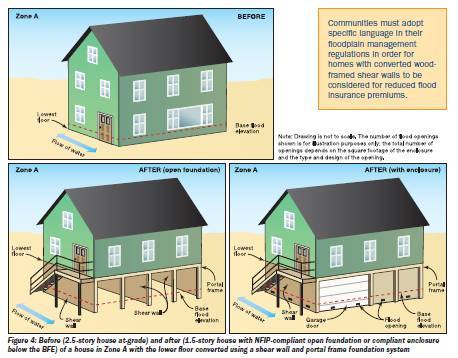

Flood construction conversionBarring any meaningful change in human behavior, the insurance industry likely will focus its attention on damage prevention. For example, many homes that are being rebuilt in areas wiped out by Superstorm Sandy are elevated and have the core mechanical systems located above predictable water levels.

Even in Portland, Maine, the soon-to-be opened Marriott Courtyard on Commercial Street will have its power plant 14 feet above the high tide mark should sea levels rise along the city’s historic waterfront.

For businesses and homeowners located near the coast or along waterways, taking measures to redesign and fortify foundations as well as elevating heating and electrical systems could pay dividends. Should we worry here in Maine and New Hampshire? The Great Hurricane of 1938 that ripped its way up the Connecticut River Valley killed an estimated 700 people and caused the loss of 57,000 homes worth $4.7 billion in today’s dollars. Also, consider that by the time Hurricane Irene (2011) became little more than a drenching tropical storm, it nevertheless caused hundreds of millions of dollars worth of damage within rural Vermont and New Hampshire.

Conclusion: Do your part to not adversely impact the environment but as important, take steps to minimize potential property losses when planning new buildings, additions or renovations.

Illustrations from FEMA.GOV (RA7, November 2013)